By: Bryce Coward, Wealth Management Advisor & Director of Investments

Inflation has undoubtedly been a dominant theme this market cycle as COVID and a complete shutdown of the economy and supply chains was followed by one of the largest stimulus packages the world has ever seen.

In the United States, consumer price inflation (CPI) peaked at about 9% in June of 2022 and has experienced nine consecutive quarters of moderation since then.[1] Most recently, the September CPI declined to 2.4% year-over-year from 2.6% in August.[2]

Looking ahead, are we to expect more dramatic disinflation with CPI settling in at 2% or below, or something else? An examination of recent data suggests we may be in the midst of an uptick inflation that has the potential to impact markets.

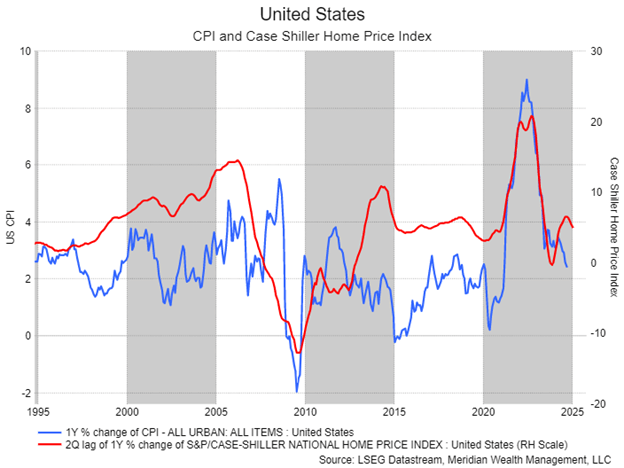

- Given the weight of housing prices in the CPI basket, CPI inflation is heavily influenced by changes in housing prices, with a lag of four to six months. The Case Shiller National Home Price Index rose by 6.5% in the first nine months of 2024, implying a tailwind to inflation through the remainder of the year and into 2025, as relatively stale CPI inflation data incorporates the previous rise in home prices.[3]

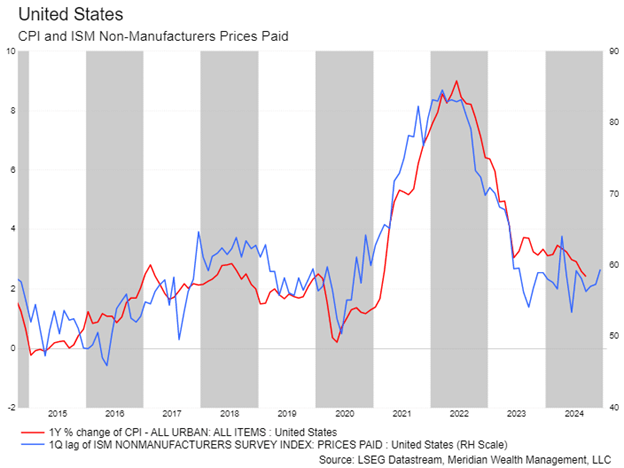

2. Businesses are still feeling the inflation pinch and attempting to pass those costs to end customers. The ISM Non-Manufacturing Index, a survey of services businesses, most recently indicated increasing prices for services.[4] The ISM Non-Manufacturing Index tends to lead the CPI by a one to two quarters.

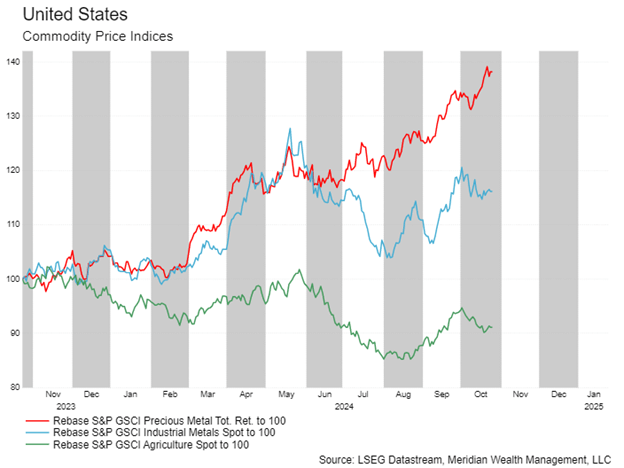

3. Broad commodity prices have risen since August.[5]

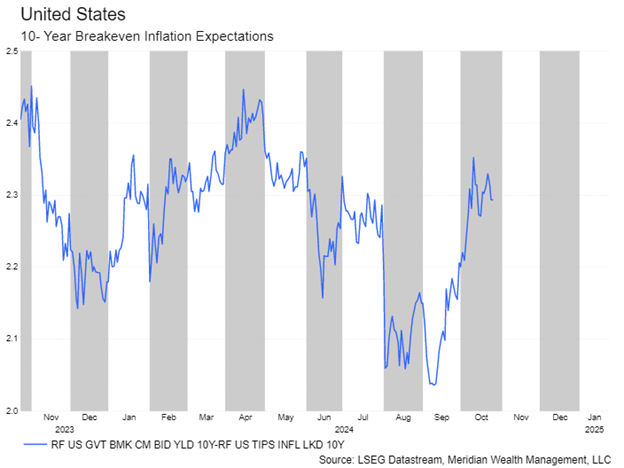

4. Market-based measures of inflation are rising again. Market-based measures of inflation are interesting insofar as they provide a more real-time gauge of inflation than economic statistics. 5-year forward inflation as priced by the US bond market has risen by .26% between September 11, 2024 and October 25, 2024.[6]

What could a reacceleration of inflation mean for capital markets?

- Possibly higher for longer bond yields. To be clear, the data may not imply a significant reacceleration of inflation that would derail the economic expansion or a Fed’s cutting cycle. However, even a modest reacceleration of inflation has the potential to throw some cold water on the Fed’s cutting cycle, causing them to cut slower or less aggressively than they signaled at the last Fed meeting. If this comes to pass, higher bond yields across the curve could be a logical outcome.

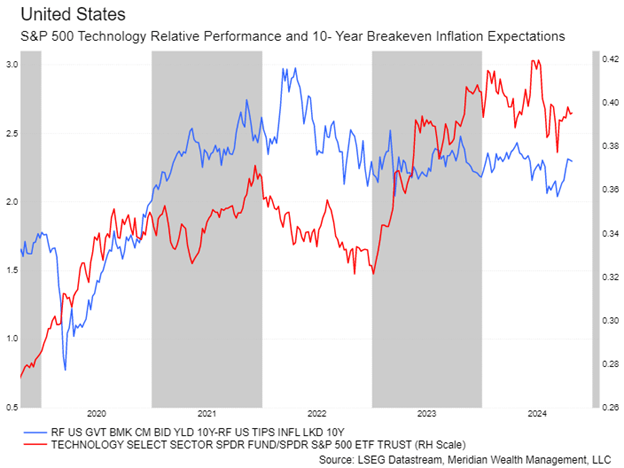

- A resumption of technology stock market leadership is another possibility. Since COVID, as inflation expectations as priced by the bond market have risen, technology has tended to outperform the broad market (red line in the chart below), presumably as market participants gravitate toward quality. Since September 10th, when 10-year inflation expectations started to rise, tech stocks have outperformed the broad market.[7]

[1] Bureau of Labor Statistics, LSEG as of 9/30/2024

[2] Bureau of Labor Statistics, LSEG as of 9/30/2024

[3] Bureau of Labor Statistics, Case Shiller, LSEG as of 9/30/2024

[4] Institute for Supply Chain Management, LSEG as of 9/30/2024

[5] GSCI, LSEG, as of 10/25/2024

[6] LSEG as of 10/25/2024

[7] LSEG as of 10/25/2024