By: Bryce Coward, Wealth Management Advisor & Director of Investments

As your trusted advisors and amid the heightened volatility in the equity markets, we wanted to reach out with our thoughts and perspective on the investment landscape. Since February 24th, 2025, the US stock market as measured by the S&P 500 is down roughly 8.8% and the tech-heavy Nasdaq 100 is down 12.5%. The correction has been attributed to uncertainty around the implementation of tariffs and a possible slowdown in economic growth or corporate earnings growth over time.

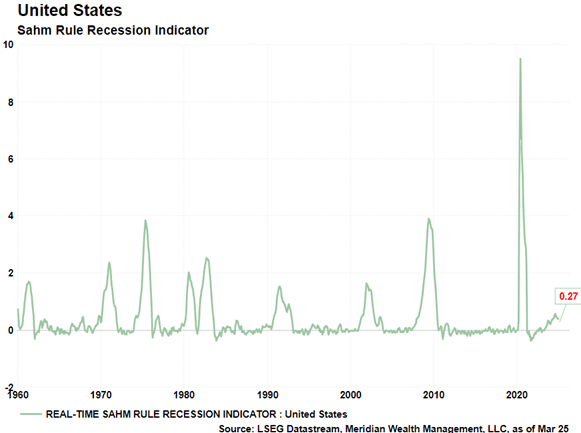

However, at this point, our expectation remains that the US economy will avoid a recession in 2025, and that heightened volatility may provide opportunities to rebalance portfolios as the year progresses. For one, the probability of recession as measured St. Louis Fed’s Sahm Real-time Recession indicator remains at a relatively low level, and has actually been declining since August 2024[1]. It may rise quickly if the labor market begins to deteriorate, but so far, the unemployment rate remains at 4.1%, an historically low level.

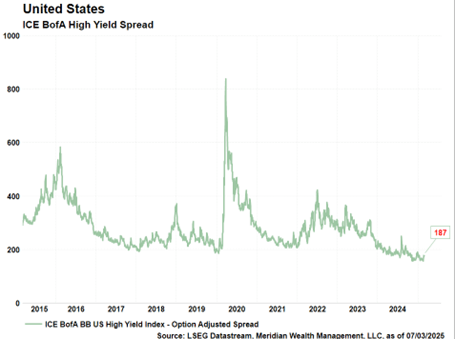

At present, the credit markets are also not signaling recession either, in our view. Typically, if the bond market is worried about a recession, and subsequent increases in defaults on bonds, credit spreads (the yield difference between a bond with credit risk and an otherwise similar Treasury bond) would begin to widen aggressively. Even in the riskier corners of the bond market (i.e. high yield bonds), credit spreads remain at very low levels (source: Bureau of Labor Statistics as of 3/7/2025).

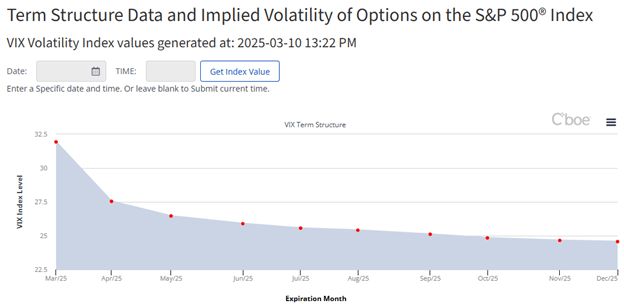

Equities, on the other hand, are stressed, in our view. One measure of stress in stocks is the VIX Index, a measure of implied volatility of the S&P 500. The VIX rises and falls based on the price of options tied to the Index. As market participants get more worried about downside protection, the price of protective options rises and so too does the VIX. Currently, not only has the VIX spiked in recent days (indicating pricier downside protection), the near-term VIX contracts have become more expensive relative to contracts that expire later in the year. In other words, investors are paying up for protection, NOW, even though the cost of said protection has skyrocketed.

An inverted VIX futures curve, which is what we have today, is 1) unusual historically, 2) may indicate that sentiment has swung too far in the bearish direction, and 3) may help support some kind of mean reverting rally over the coming days and weeks. Indeed, over the last 10 years, the VIX curve has been inverted only 16% of the time.The average 12-month An inverted VIX futures curve, which is what we have today, is 1) unusual historically, 2) may indicate that sentiment has swung too far in the bearish direction, and 3) may help support some kind of mean reverting rally over the coming days and weeks. Indeed, over the last 10 years, the VIX curve has been inverted only 16% of the time. The average 12-month forward return following those VIX curve inversions was 21.25% vs 10.54% for non-inverted days (source: LSEG, Meridian Wealth Management as of 3/10/2025).

Bonds as Protection?

While the equities have been selling off, at least one asset class has held its own. After a 4-year bear market, the bond market has, for the first time this cycle, provided some level of diversification to equity risk. Indeed, since the beginning of the year, the US 10 Year Treasury yield has fallen from 4.79% on January 14th to 4.22% as of 3/10/2025. It may not seem like much, but that equates to roughly a 3.8% rise in value during a time when stocks are down nearly 10%. As a risk management and diversification measure, we began lengthening maturities in our active bond strategies last Fall.

Long-term investing

Seasoned investors are all-too familiar with market volatility. Indeed, the 8.8% decline in the S&P 500 is nothing compared to the 22% decline in 2022, the 35% COVID waterfall in March of 2020, the 20% Taper Tantrum December 2018, the 20% manufacturing recession of 2015-2016, the 20% “double dip” sell off 2011, or the 54% Great Financial Crisis. Yet, this correction feels different. Maybe it’s our attention to news? Maybe it’s the orientation of the Earth relative to the Sun. Who cares. Volatility is volatility and we suspect very few people like it when the stock market goes down.

As advisors and investors, we have several levers to pull when it comes to managing the wealth of our clients:

- Security selection – skewing towards what we believe are higher quality investments

- Diversification – spreading the bets out in order to reduce exposure to any one risk factor, event, company, etc.

- Asset allocation – tuning in the exposure between the various asset classes, again, in an effort to reduce risk where appropriate while also attempting to achieve other goals, be they growth, income, etc.

And then there is time. Stocks go up and down. Interest rates go up and down. Historically, and perhaps especially in times of stress, capital markets have tended to create more wealth than they have destroyed. This may be especially true for those with the patience to let security selection, diversification, and asset allocation work for them as the pendulum eventually swings the other way.

Sincerely,

Your Meridian Wealth Management Advisory team