Labor market data sits at the center of how people judge the health of the economy. It’s one of the most widely cited indicators of economic strength, and also one of the most emotionally charged. Jobs aren’t abstract. They’re concrete. They shape income, identity, and facilitate a sense of security, which makes labor headlines especially powerful because of their emotionally charged nature.

Over the past year, steady commentary has pointed to rising unemployment, slowing hiring, and high-profile layoff announcements as evidence that the labor market is on the verge of breaking. That interpretation is understandable, but it’s also incomplete. Labor data is easy to misread when individual data points are viewed in isolation or through the lens of fear rather than context.

What the data actually shows is not a labor market in distress, but one that is cooling in an orderly way after an unusually tight post-pandemic period. Below, is a breakdown of what’s softening, what’s holding up, and why fears of an imminent labor-market break are likely overblown.

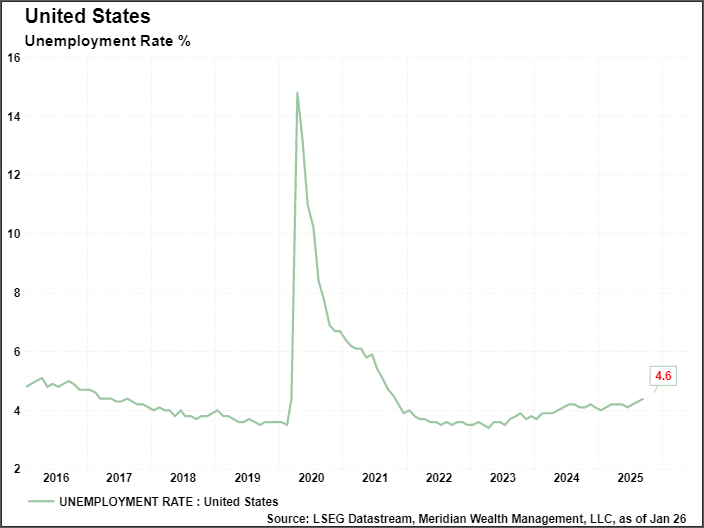

Unemployment: Drifting Higher, Not Spiking

The unemployment rate has risen from 4.2% in November 2024 to 4.6% in November 2025 (Bureau of Labor Statistics, Employment Situation, as of Nov 2025). A 0.4-percentage-point increase over a year is meaningful, but it’s far from recessionary. Historically, unemployment tends to rise by 1.0–1.5 percentage points before recessions take hold.

The key nuance: unemployment is rising without a corresponding surge in layoffs. That distinction matters.

Job Creation: Slower, With Soft Spots Emerging

Payroll growth has cooled substantially. Several months in late 2025 showed flat or slightly negative job creation, and public reporting based on Bureau of Labor Statistics (BLS) data indicates the economy has shed roughly 40,000 jobs since September 2025 (as of Dec 2025).

Softer areas include:

- Interest-rate-sensitive sectors including construction, manufacturing, and durable goods have slowed as persistently high borrowing costs weigh on demand

- Professional and business services, hiring has decelerated as companies shift from expansion to a focus on profit margins

- Transportation and warehousing, a post-pandemic normalization in goods demand has reduced the need for incremental labor

These pockets of softness align with broader macro trends: slightly tighter financial conditions, slower goods consumption, and a corporate pivot toward cost control.

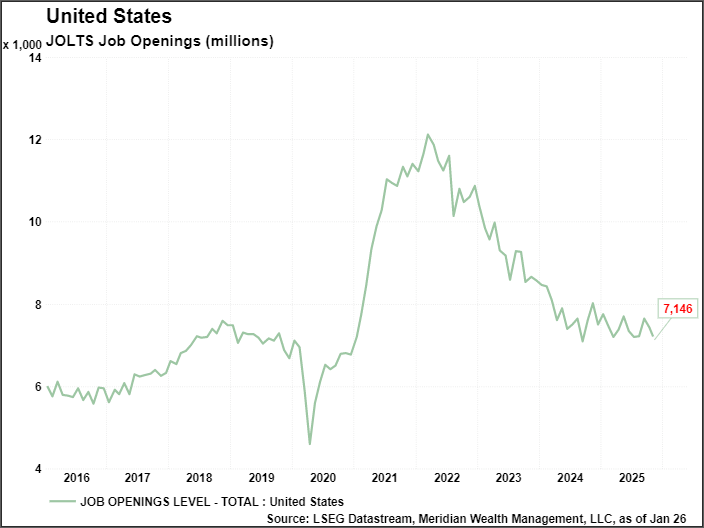

Job Openings: Down From the Peak, but Still Elevated

The Job Opening and Labor Turnover Survey (JOLTS) by BLS report shows 7.7 million job openings in October 2025. That’s well below the 12-million peak of 2022, but still above pre-pandemic norms.

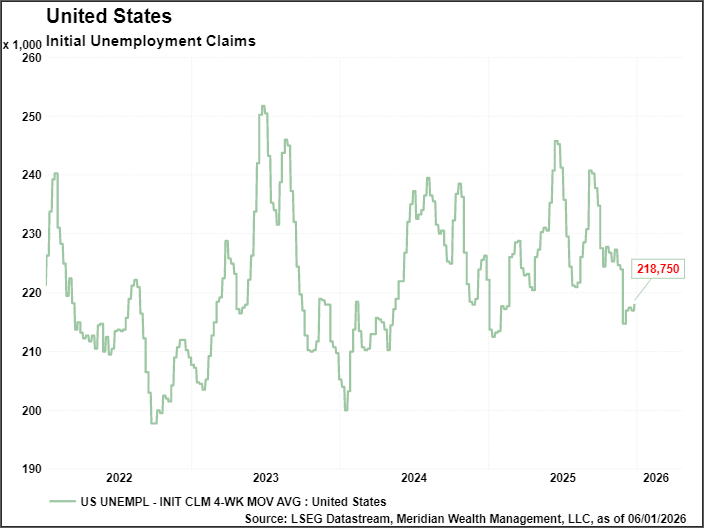

This is a classic “cooling, not collapsing” pattern, which is also supported by a relatively low level of initial unemployment claims. Indeed, as of the last week of December initial claims tallied 199,000 – the second-lowest reading in two years, according to the U.S. Department of Labor, as of Dec 27, 2025.

Layoffs Aren’t Driving the Slowdown

One of the clearest signals that the labor market is cooling rather than breaking is the behavior of initial unemployment claims. Despite a gradual rise in the unemployment rate and slower hiring, claims remain historically low. That matters because claims are the most direct real-time indicator of layoffs. When labor markets crack, claims surge quickly and broadly. That simply isn’t happening.

This divergence, higher unemployment alongside low claims, suggests employers are responding to slower demand by pulling back on hiring rather than cutting existing workers. In other words, labor market adjustment is occurring through restraint, not stress.

What Could Shape Labor Markets in 2026

As to move into 2026, we anticipate:

- elevated tax refunds compared to 2025

- a continued accommodative Fed with more interest rate cuts in the offing, and

- an anchoring of investment in AI capacity.

In our view, these features argue for the unemployment rate to continue to drift modestly higher while avoiding a spike consistent with a recession.

Why Labor Data Matters for Long-Term Investors

Labor market data matters because it influences many of the forces that ultimately shape long-term outcomes—corporate earnings, consumer demand, interest-rate policy, and, over time, asset prices. A labor market under stress can create feedback loops that weigh on growth and profitability, which is why it’s closely watched.

Yet not every rise in unemployment or slowdown in hiring carries the same implications. What ultimately matters is whether labor weakness becomes broad, persistent, and self-reinforcing. The current data does not point in that direction. Instead, it reflects an economy adjusting from an unusually tight post-pandemic labor market toward more sustainable conditions.

For long-term investors, the greater risk often lies not in economic cooling itself, but in reacting to emotionally charged signals without sufficient context. Labor data can influence markets, but it does not override the fundamentals that drive long-term returns: productivity, earnings growth, innovation, and capital discipline.

Advisory services offered through Meridian Wealth Management, LLC, a Registered Investment Advisor. Seek tax, legal, insurance, and investment advice from a licensed professional relative to your situation. The information and opinions voiced in this material are strictly for general information only and are not intended to provide any security recommendations, specific advice, or recommendations. All investing involves risk, including loss of principal. Past performance does not guarantee future results.